A.R. is a high tech professional in his early 40s who quickly saw how an HSA could help him pay for medical expenses tax-free. Learn why he thinks health and retirement planning is essential and the role HSAs play in that.

SO: How did you find out about health savings accounts (HSAs)? How did they benefit you?

I had always assumed that a PPO provided the best care, policy, and coverage. Just from the apprehension of having a large bill and having any sort of stability and predictability of planning in my health planning, I had always considered using a PPO.

A couple of years back, there was a large push at my current employer to highlight the additional benefits that a health savings account (by using a High Deductible Health Plan–HDHP) provided. Also, my financial planner recommended looking into it, but there was never a strong push from them.

I started looking into details of the plan, trying to understand the incentive that my current employer had provided.

The first three factors got me researching it. The additional factor of contributions that the employer did and finally my own situation and where I am from a health perspective made me realize that this is where I need to be.

SO: Do you look at this as a tax-free retirement vehicle or do you look at this as a tax-free cash account for medical expenses?

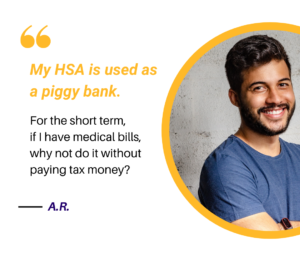

The latter. My HSA is used as a piggy bank. We should always be thinking about retirement. But when I think about retirement, I think about my other accounts. So, this doesn’t play a big role. For the short term, if I have medical bills, why not do it without paying tax money?

SO: Was the information provided to you by your employer, outside of direct money going into your account, useful, sufficient, or a good starting point for more research?

To get to the point where you understand there is an option is really relevant. Also, how it was advertised played a role. For the most part, I don’t need medical coverage, but the moment you say there is a savings account associated with it, the conversation changes. You say, “Wait, I can save more money, pay less taxes, and get benefits on medical?”

SO: What advice would you give someone who is just starting out on their HSA journey?

It’s an excellent program. It doesn’t matter if you are a high net worth individual or mid net worth, take an assessment, and understand where your health is with your own family.

If you are looking at health planning, that should be a big part of what you do every year. So it’s not only about putting money in college funds. This has to become front and center type of that type of planning.

Think about the long term benefits you would get–especially if you are thinking about retiring in the United States. And as you grow older, you might have future expenses that this plan and this compound interest can actually benefit you with.

SO: Was there something that you wish someone had told you when you were just starting out on retirement planning?

I started my retirement planning when I was 21. It’s important to be financially independent. I grew up with that idea. So when I think about retirement planning, I am probably in the rare category of folks that think about it at ages 17 or 18. In that way, better understanding the importance of compound interest, market fluctuations, and long term strategy. At that time, if I had understood those things better, I would have gone beyond just 401(k) and taken advantage of more accounts.

SO: Did you have any mindset barriers to overcome when you were starting out?

Yes, basically that I wasn’t going to see this money for a long, long time. I needed to balance the lifestyle that I live with understanding the importance of this. To get over the mindset barrier, I had to realize that the money is available to me in the future and also available to me in excruciating circumstances. Money is there. Money is growing.

It also helped me set a tone for how I am going to live my life. Where am I going to spend money and where am I not going to spend money? It wasn’t a linear growth where I said, “well, I’m making more, so I’m going to spend more.” I set up a threshold independent of where my salary grows. Anything else I make goes directly into retirement or investment.

NOTE: These are edited excerpts from the conversation with an HSA participant. In some cases, stock photos and only first names or initials have been used to protect identity.